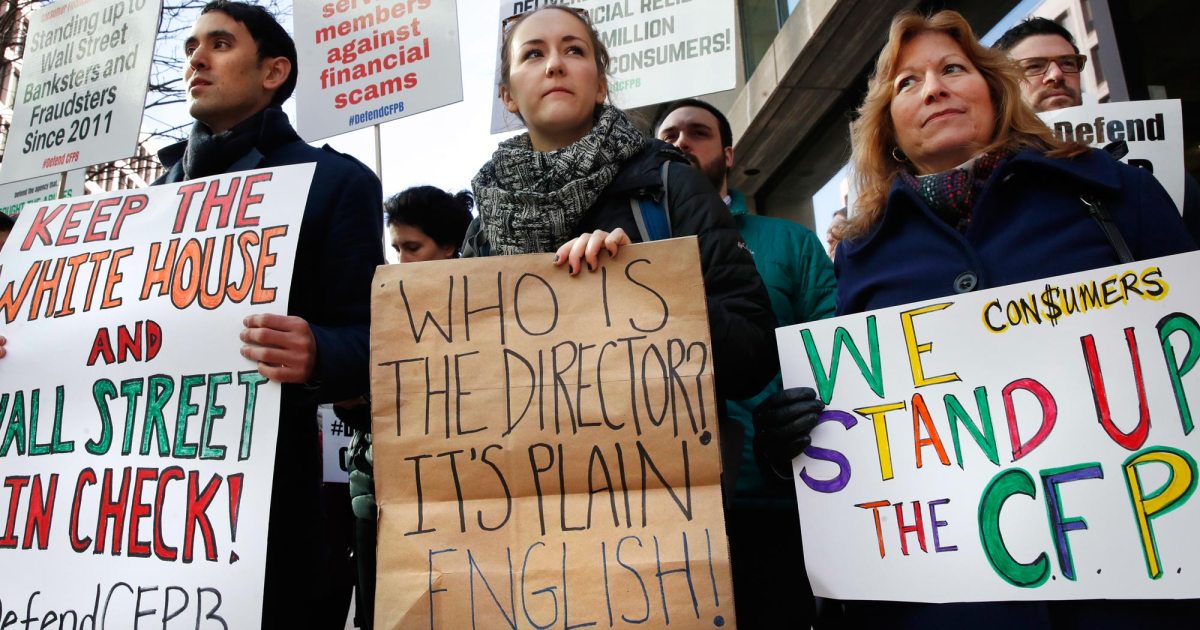

I don’t recall Donald Trump saying during the presidential campaign that he planned to make his supporters helpless against predatory lenders and financial scam artists, but that is apparently what he is about to do at the Consumer Financial Protection Bureau. Trump has ousted CFPB director Rohit Chopra, a zealous champion of consumer protection, and given control of the agency to Scott Bessent, the former hedge fund manager who is already serving as Treasury Secretary.

Bessent’s first act was to order a halt to all activities at the CFPB, including rulemaking and enforcement. He issued a statement saying: “I look forward to working with the CFPB to advance President Trump’s agenda to lower costs for the American people and accelerate economic growth.” Translation: I will slash regulation and perpetuate the myth that reduced oversight works to the benefit of consumers.

The firing of Chopra and freezing of CFPB activities come as welcome news to major financial institutions and fly-by-night operators, both of which have sought to neutralize the agency ever since it began operation in 2011. The agency was also a frequent target of criticism from Congressional Republicans, who hated the fact that the law creating the CFPB provided that the director could only be removed for cause. In 2020 the conservative majority of the Supreme Court threw out that provision, meaning that the director could be removed at will by the President.

As shown in Violation Tracker, the CFPB has over its life collected more than $17 billion in fines and settlements, much of which has gone to affected consumers in the form of restitution. The cases, numbering more than 250, have involved a wide range of financial misconduct, from the Wells Fargo bogus account scandal to the deceptive practices of for-profit colleges.

Let’s focus on one subset of cases in which the CFPB has been especially active: cases brought against lenders that prey on military families. The agency has collected more than $146 million in penalties in a dozen such cases. A big share of that total comes from a $92 million settlement reached in 2014 with Colfax Capital and Culver Capital, also known as Rome Finance. The case, brought in cooperation with 13 state attorneys general, accused Rome Finance of luring servicemembers with the promise of instant financing on expensive electronics but then masked the finance charges with inflated prices in marketing materials and later withheld key information on monthly bills. Richard Cordray, CFPB’s director at the time, stated: “Rome Finance’s business model was built on fleecing servicemembers.”

In 2023 the CFPB found that TMX Finance, known as TitleMax, violated the Military Lending Act by extending prohibited title loans to military families, often charging nearly three times more than the 36% annual interest rate cap. The agency said TitleMax tried to hide its unlawful activities by, among other things, altering the personal information of military borrowers to circumvent their protected status. The CFPB also found that TitleMax increased loan payments for borrowers by charging unlawful fees. The agency ordered the company to pay more than $5 million in consumer relief and a $10 million civil money penalty.

Large financial institutions have also been called out by the CFPB for cheating military families. U.S. Bank and one of its nonbank partner companies, Dealers’ Financial Services, were required to return about $6.5 million to servicemembers for failing to properly disclose all the fees charged to participants in the companies’ Military Installment Loans and Educational Services auto loans program, and for misrepresenting the true cost and coverage of add-on products financed along with the auto loans.

Those who would eliminate or defang the CFPB—especially those who take every opportunity to express their support for the troops–should be made to made to acknowledge that their actions will make military families, as well as millions of others, more vulnerable to financial predators.

The world according to Trump is one of grievances and victimhood. During the presidential campaign he got a lot of mileage by appearing to empathize with the travails of the white working class and promising to be their champion in fighting against the impact of globalization and economic restructuring. At times he even seemed to be adopting traditional left-wing positions by criticizing big banks and big pharma.

The world according to Trump is one of grievances and victimhood. During the presidential campaign he got a lot of mileage by appearing to empathize with the travails of the white working class and promising to be their champion in fighting against the impact of globalization and economic restructuring. At times he even seemed to be adopting traditional left-wing positions by criticizing big banks and big pharma. Trump’s travel ban and his rightwing Supreme Court pick are troubling in themselves, but they are also serving to deflect attention away from the plot by the administration and its Republican allies to undermine the regulation of business.

Trump’s travel ban and his rightwing Supreme Court pick are troubling in themselves, but they are also serving to deflect attention away from the plot by the administration and its Republican allies to undermine the regulation of business. Reincorporating in foreign countries with lower tax rates is not the only way large corporations put profit before patriotism. A

Reincorporating in foreign countries with lower tax rates is not the only way large corporations put profit before patriotism. A  Every industry has its faults, but there are only a few for which it can be said that society would be better off if they did not exist at all. One member of that special group is payday lending, the business of providing short-term cash advances to desperate people at unconscionably high interest rates with the expectation that they will not be able to repay the money and thereby get caught in an ever-worsening debt trap.

Every industry has its faults, but there are only a few for which it can be said that society would be better off if they did not exist at all. One member of that special group is payday lending, the business of providing short-term cash advances to desperate people at unconscionably high interest rates with the expectation that they will not be able to repay the money and thereby get caught in an ever-worsening debt trap. The business news has been full of speculation on whether JPMorgan Chase Jamie Dimon will go on serving as both CEO and chairman of the big bank, in light of a shareholder campaign to strip him of the latter post. The effort to bring Dimon down a notch—and to oust three members of the board—is hardly the work of a “lynch mob,” as Jeffrey Sonnenfeld of Yale

The business news has been full of speculation on whether JPMorgan Chase Jamie Dimon will go on serving as both CEO and chairman of the big bank, in light of a shareholder campaign to strip him of the latter post. The effort to bring Dimon down a notch—and to oust three members of the board—is hardly the work of a “lynch mob,” as Jeffrey Sonnenfeld of Yale  Undeterred by its eviction from public parks in numerous cities, the Occupy movement is looking to other venues, among them college campuses.

Undeterred by its eviction from public parks in numerous cities, the Occupy movement is looking to other venues, among them college campuses.

You must be logged in to post a comment.